The health of a real estate market can be measured in multiple ways. Today, our study will be derived from two data sets: 1) the prices -median and range- and 2) the number of transactions over time. Our research bears exclusively on the beachfront houses located in 30A, from Rosemary Beach (East) to Stallworth (West). The data is drawn monthly and quarterly since January of 2020 – the onset of the Covid pandemic.

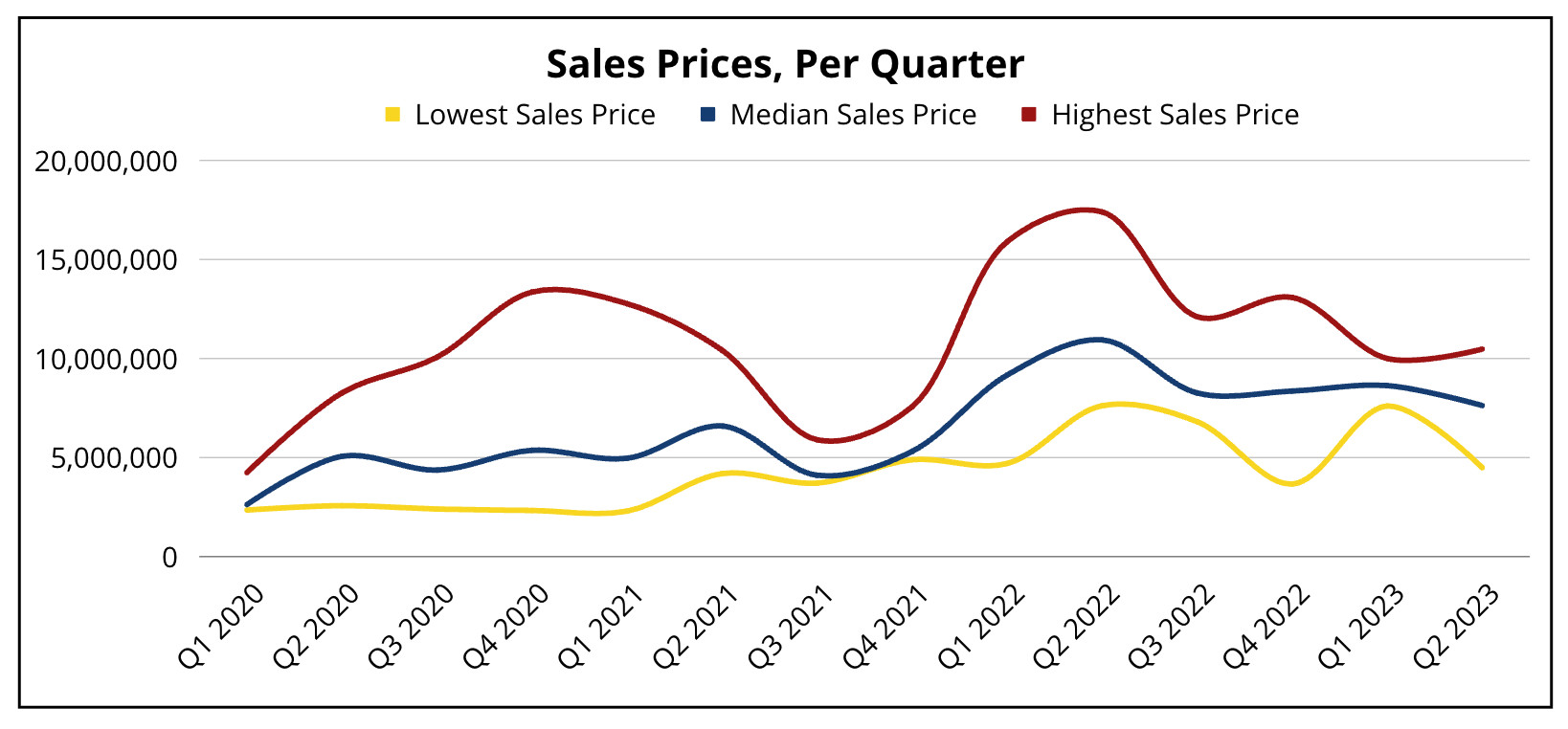

Median and Range

Median and Range

We should note that, although the Median sales price is the most significant information, the range and especially the variation over time of the most expensive sales tend to amplify the trend displayed by the Median. The highest sale, when tracked monthly, gives a good indication of the market progression.

The strong value increases of 2020/2021 are depicted in the growth of the Median curve from 2020-Q1 until 2021-Q2. Then, 2021-Q3 and -Q4 show a reduction in the Median prices. It is important to note that a decrease in the Median price means that the buyers’ appetite turned to more ‘modest’ homes; it does not mean that the value of a given home went down during the period – actually, quite to the contrary, prices kept moving up. The first two quarters of 2022 displayed a robust increase in the Median prices. From 2022-Q3 until 2023-Q2, after a quick decrease in value, Medians have stabilized. This most recent phase has been driven by higher interest rates.

Noteworthy, July 2023 has outperformed the first half of the year in raising the highest sale from about $11 million to $14.5 million. The Median remained stationary, due to the sustained high interest rates… but strong buyers are coming back to the area, motivated by good news surrounding the economy.

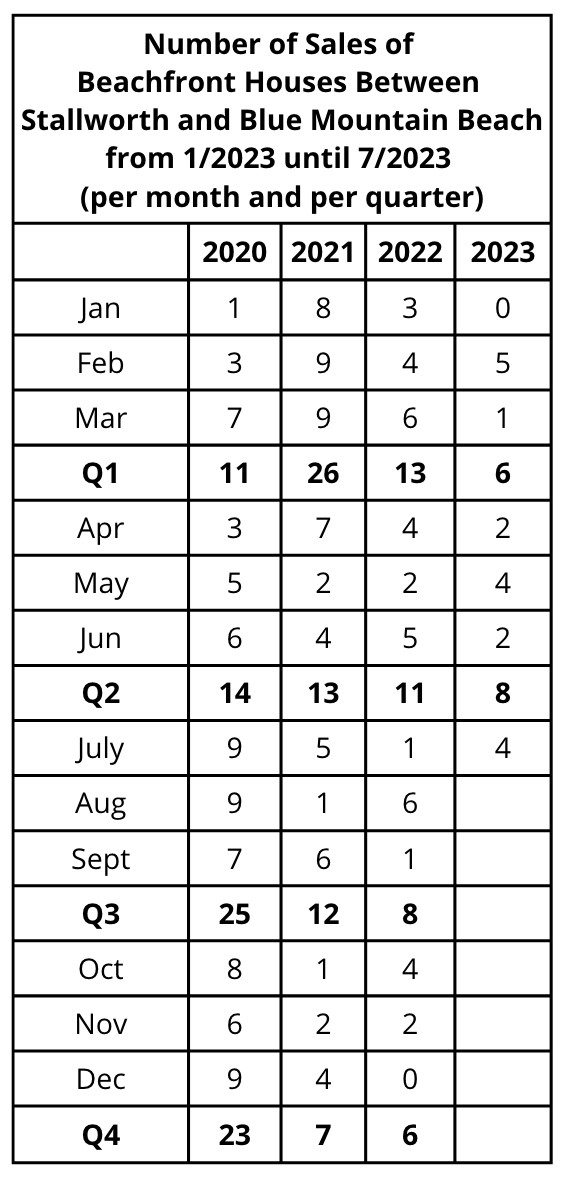

Number of Sales, From January 2020 and until July 2023 (monthly and quarterly)

The consensus pertaining to Florida real estate is that: (1) the market was non-existent during the first months of Covid – this is confirmed by the results of 2020-Q1. (2) From the time Florida reopened during Covid in April 2020 until 2021-Q2, sales were strong – this too is verified with our local market’s data. (3) Then, sales remained healthy until 2022-Q2. (4) Since interest rates started increasing in mid-2022, and markedly during 2022-Q3, the activity has slowed down – this too bears truth for our specific market.

Generally, the first quarter of the year (Q1) is expected to bring approximately 13 sales. The second quarter (Q2), slightly less with 12 sales. The third quarter (Q3), 9. The fourth quarter (Q4), 7.

These general trends are confirmed by the graph: (1) the most active period is the first half of the year, quarters Q1 and Q2 from January until June, (2) the last quarter of the year is the slowest, (3) and general market conditions can greatly amplify or diminish the expected average numbers.

From 2022-Q3 through 2023-Q2, the numbers of sales have been disappointing. The question that matters is: Is this sleepy situation likely to last or should we expect an uptick in activity? We will answer the question objectively and subjectively. Subjectively first. The inventory ‘for sale’ has been at its lowest for one year. With little choice, opportunities dwindle for buyers; consequently, fewer purchases happen. This situation has led to a regular increase in property values, coupled with a paucity of sales. As we are entering the slow sales period of the year, July 2023’s data bears importance to anticipate the performance for the rest of the year. In the past years, July has registered the highest variation in sales numbers, from 9 in 2020 at the peak of the Covid-driven demand to 1 last year in 2022. The 4 sales in July 2023 reflect a normal-to-healthy market and represent a step in the direction of normalcy.

Conclusion

In conclusion, we seem to leave behind us the timid markets of the post-Covid/high-interest-rate era of 2022 and first half of 2023. We navigate in waters where more transactions are closed – going back to a normal level. Prices have shown no signs of abatement. This too is a positive omen. As of August 2023, it appears that the second half of 2023 will be strong.